All Categories

Featured

Table of Contents

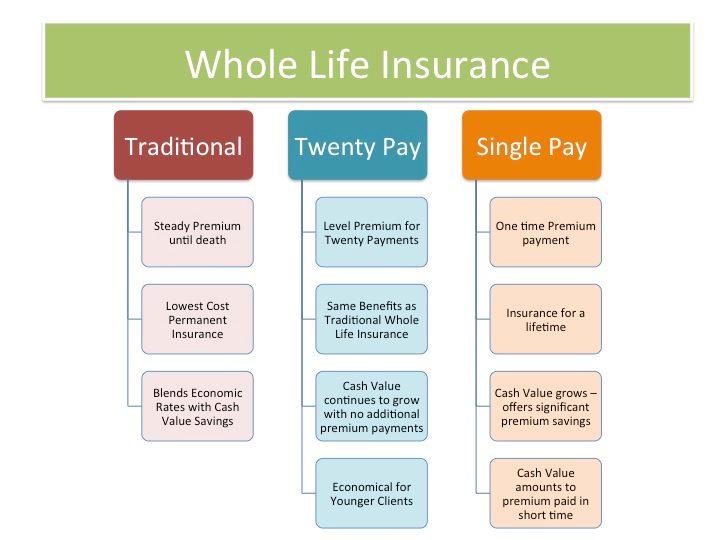

The are entire life insurance and universal life insurance. expands cash money worth at a guaranteed rates of interest and additionally via non-guaranteed dividends. grows cash value at a dealt with or variable price, relying on the insurance firm and plan terms. The cash money value is not contributed to the survivor benefit. Cash money value is a feature you make the most of while alive.

The plan lending passion price is 6%. Going this course, the passion he pays goes back into his plan's money worth rather of a financial institution.

How To Set Up Infinite Banking

Nash was a money specialist and follower of the Austrian institution of economics, which supports that the value of goods aren't explicitly the outcome of traditional financial structures like supply and demand. Rather, individuals value money and goods in different ways based on their economic standing and demands.

One of the mistakes of standard financial, according to Nash, was high-interest prices on lendings. Long as banks established the passion prices and funding terms, individuals really did not have control over their very own riches.

Infinite Banking needs you to possess your economic future. For goal-oriented individuals, it can be the most effective financial device ever. Right here are the benefits of Infinite Financial: Arguably the single most advantageous element of Infinite Banking is that it boosts your cash flow. You don't need to experience the hoops of a standard bank to get a finance; merely demand a policy finance from your life insurance policy company and funds will be made readily available to you.

Dividend-paying whole life insurance coverage is really reduced risk and provides you, the insurance policy holder, a lot of control. The control that Infinite Financial supplies can best be grouped into two groups: tax advantages and property defenses - life insurance from bank. One of the reasons entire life insurance policy is suitable for Infinite Financial is how it's tired.

Infinite Banking Concept Scam

When you utilize entire life insurance policy for Infinite Banking, you become part of a personal contract between you and your insurance provider. This privacy provides particular possession protections not discovered in other monetary automobiles. Although these securities may differ from state to state, they can consist of defense from asset searches and seizures, defense from judgements and protection from lenders.

Entire life insurance policy policies are non-correlated assets. This is why they function so well as the financial structure of Infinite Banking. Despite what takes place in the market (supply, genuine estate, or otherwise), your insurance coverage retains its well worth. A lot of individuals are missing this crucial volatility buffer that helps secure and grow riches, instead dividing their cash right into 2 pails: checking account and investments.

Whole life insurance coverage is that third bucket. Not only is the price of return on your whole life insurance coverage plan guaranteed, your death advantage and premiums are additionally guaranteed.

This framework lines up completely with the concepts of the Perpetual Wealth Method. Infinite Financial interest those seeking better monetary control. Right here are its main benefits: Liquidity and ease of access: Policy loans provide instant accessibility to funds without the restrictions of conventional small business loan. Tax performance: The cash worth grows tax-deferred, and policy finances are tax-free, making it a tax-efficient device for constructing wide range.

Unlimited Banking Solutions

Asset defense: In lots of states, the money worth of life insurance policy is secured from creditors, adding an extra layer of monetary protection. While Infinite Banking has its advantages, it isn't a one-size-fits-all service, and it comes with considerable downsides. Below's why it might not be the finest technique: Infinite Banking often requires complex plan structuring, which can puzzle policyholders.

Imagine never ever having to worry about financial institution finances or high interest rates once more. That's the power of boundless financial life insurance coverage.

There's no set funding term, and you have the flexibility to make a decision on the settlement timetable, which can be as leisurely as settling the finance at the time of fatality. This flexibility includes the maintenance of the loans, where you can go with interest-only payments, keeping the financing equilibrium level and convenient.

Holding money in an IUL taken care of account being credited interest can usually be better than holding the cash on deposit at a bank.: You have actually constantly desired for opening your very own bakeshop. You can obtain from your IUL policy to cover the first expenses of renting out a room, acquiring tools, and employing personnel.

Bank Of China Visa Infinite

Personal financings can be acquired from standard banks and credit scores unions. Here are some bottom lines to think about. Credit score cards can provide a versatile method to obtain cash for extremely short-term periods. Borrowing cash on a debt card is generally extremely costly with yearly percent prices of rate of interest (APR) often getting to 20% to 30% or even more a year.

The tax treatment of plan car loans can differ significantly depending on your country of home and the particular regards to your IUL plan. In some areas, such as North America, the United Arab Emirates, and Saudi Arabia, plan loans are typically tax-free, offering a considerable advantage. However, in various other territories, there may be tax obligation implications to consider, such as possible tax obligations on the car loan.

Term life insurance policy only gives a death advantage, without any type of cash money worth accumulation. This indicates there's no money worth to obtain against. This post is authored by Carlton Crabbe, President of Resources for Life, an expert in supplying indexed universal life insurance policy accounts. The details provided in this post is for educational and informational purposes just and ought to not be understood as monetary or financial investment advice.

However, for funding police officers, the comprehensive guidelines imposed by the CFPB can be viewed as difficult and restrictive. Initially, lending police officers frequently argue that the CFPB's regulations produce unnecessary bureaucracy, bring about more documentation and slower lending processing. Regulations like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) requirements, while aimed at protecting customers, can result in hold-ups in shutting deals and raised operational prices.

{kind=link}

Latest Posts

Hybrid Debt & Mortgage Arbitrage, Become Your Own Bank

Be Your Own Bank: Practical Tips

Non Direct Recognition Life Insurance Companies