All Categories

Featured

Table of Contents

Okay, to be reasonable you're really "financial with an insurance provider" instead of "banking on yourself", yet that idea is not as simple to offer. Why the term "boundless" financial? The idea is to have your cash functioning in several areas at the same time, rather than in a solitary area. It's a bit like the concept of buying a residence with cash, after that obtaining versus the house and putting the cash to operate in an additional financial investment.

Some individuals like to chat concerning the "rate of money", which generally indicates the same point. That does not suggest there is nothing worthwhile to this principle once you obtain past the advertising and marketing.

The whole life insurance policy market is afflicted by overly costly insurance policy, massive compensations, dubious sales techniques, low prices of return, and poorly informed clients and salespeople. Yet if you wish to "Rely on Yourself", you're mosting likely to need to fall to this sector and really buy whole life insurance policy. There is no replacement.

The guarantees intrinsic in this product are essential to its feature. You can obtain versus most kinds of cash money value life insurance policy, yet you shouldn't "financial institution" with them. As you acquire an entire life insurance plan to "bank" with, remember that this is a completely separate area of your economic strategy from the life insurance policy section.

Get a large fat term life insurance policy plan to do that. As you will see below, your "Infinite Financial" plan actually is not mosting likely to accurately offer this vital financial feature. Another trouble with the fact that IB/BOY/LEAP relies, at its core, on a whole life plan is that it can make acquiring a policy bothersome for much of those thinking about doing so.

Infinite Banking Think Tank

Hazardous hobbies such as diving, rock climbing, sky diving, or flying additionally do not blend well with life insurance coverage products. The IB/BOY/LEAP advocates (salesmen?) have a workaround for youbuy the plan on someone else! That might exercise fine, considering that the point of the policy is not the fatality advantage, but keep in mind that purchasing a plan on small kids is extra expensive than it needs to be because they are normally underwritten at a "common" rate as opposed to a liked one.

A lot of policies are structured to do one of two things. The majority of commonly, policies are structured to make best use of the payment to the agent marketing it. Negative? Yes. Yet it's the truth. The payment on an entire life insurance policy is 50-110% of the first year's costs. Occasionally policies are structured to maximize the survivor benefit for the costs paid.

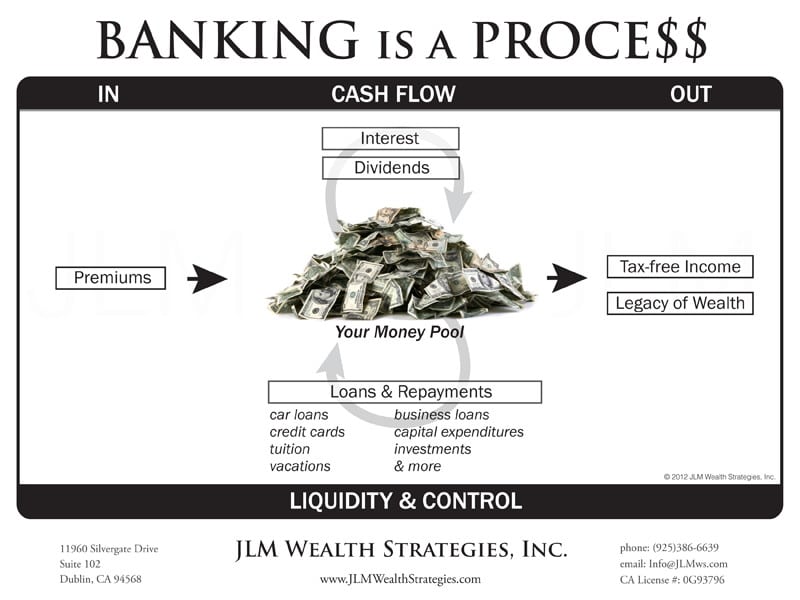

With an IB/BOY/LEAP policy, your goal is not to make best use of the survivor benefit per dollar in costs paid. Your goal is to make best use of the money worth per dollar in costs paid. The price of return on the policy is very vital. Among the most effective ways to make best use of that element is to obtain as much cash money as feasible into the policy.

The best method to enhance the price of return of a plan is to have a reasonably small "base plan", and then placed even more cash money right into it with "paid-up additions". With even more cash in the plan, there is even more money value left after the costs of the fatality advantage are paid.

An added benefit of a paid-up addition over a regular premium is that the payment price is lower (like 3-4% as opposed to 50-110%) on paid-up additions than the base policy. The much less you pay in payment, the higher your price of return. The price of return on your cash money worth is still going to be adverse for a while, like all money value insurance plan.

Yet it is not interest-free. As a matter of fact, it might set you back as high as 8%. The majority of insurer only provide "direct acknowledgment" financings. With a direct acknowledgment funding, if you obtain out $50K, the reward rate put on the cash money worth each year just puts on the $150K left in the policy.

Infinite Banking Illustration

With a non-direct acknowledgment loan, the business still pays the same reward, whether you have actually "borrowed the cash out" (practically against) the policy or otherwise. Crazy? Why would they do that? That understands? But they do. Commonly this function is coupled with some less beneficial facet of the plan, such as a reduced returns rate than you may get from a policy with direct recognition lendings (infinite banking video).

The business do not have a source of magic complimentary money, so what they give in one area in the plan should be drawn from an additional area. But if it is taken from a feature you care much less around and put right into a function you care a lot more around, that is a good idea for you.

There is one even more crucial feature, normally called "laundry car loans". While it is excellent to still have actually returns paid on cash you have gotten of the plan, you still need to pay interest on that lending. If the reward price is 4% and the finance is charging 8%, you're not exactly appearing ahead.

With a laundry finance, your loan rate of interest coincides as the returns price on the policy. So while you are paying 5% passion on the car loan, that interest is entirely countered by the 5% reward on the car loan. So in that respect, it acts simply like you took out the cash from a checking account.

5%-5% = 0%-0%. Without all 3 of these variables, this plan merely is not going to function really well for IB/BOY/LEAP. Almost all of them stand to profit from you acquiring right into this idea.

There are lots of insurance representatives talking regarding IB/BOY/LEAP as a function of entire life that are not in fact offering plans with the needed attributes to do it! The problem is that those who recognize the concept best have a massive dispute of rate of interest and typically inflate the advantages of the principle (and the underlying plan).

Public Bank Visa Infinite

You need to compare loaning versus your plan to withdrawing money from your savings account. Go back to the beginning. When you have absolutely nothing. No money in the bank. No money in investments. No cash in cash money worth life insurance policy. You are confronted with an option. You can place the cash in the financial institution, you can invest it, or you can get an IB/BOY/LEAP policy.

You pay taxes on the interest each year. You can save some even more cash and placed it back in the financial account to start to gain passion once again.

It expands over the years with resources gains, rewards, leas, etc. Several of that income is strained as you go along. When it comes time to get the watercraft, you offer the financial investment and pay tax obligations on your long-term capital gains. After that you can save some more money and buy some more investments.

The money value not used to pay for insurance policy and payments grows over the years at the reward price without tax obligation drag. It begins out with adverse returns, yet ideally by year 5 or so has recovered cost and is expanding at the dividend rate. When you go to buy the watercraft, you borrow against the plan tax-free.

Infinite Banking Software

As you pay it back, the money you repaid begins expanding again at the dividend rate. Those all work quite likewise and you can compare the after-tax prices of return. The fourth alternative, however, works very differently. You do not save any kind of money nor buy any kind of investment for many years.

They run your credit score and offer you a lending. You pay passion on the obtained cash to the bank until the financing is paid off. When it is paid off, you have a virtually worthless watercraft and no money. As you can see, that is nothing like the first 3 choices.

{kind=link}

Latest Posts

Hybrid Debt & Mortgage Arbitrage, Become Your Own Bank

Be Your Own Bank: Practical Tips

Non Direct Recognition Life Insurance Companies